Featured

Data Insight

Jan. 2, 2026

Newsletter

Dec. 6, 2024

Data Insight

Jun. 19, 2024

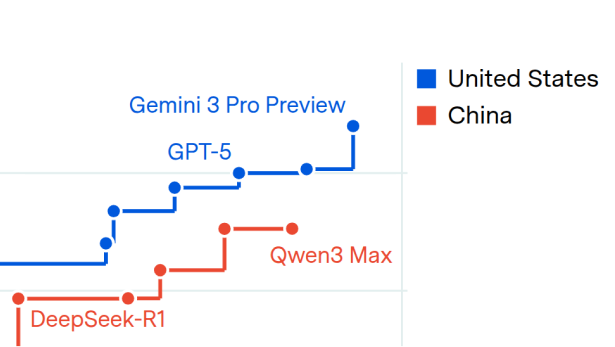

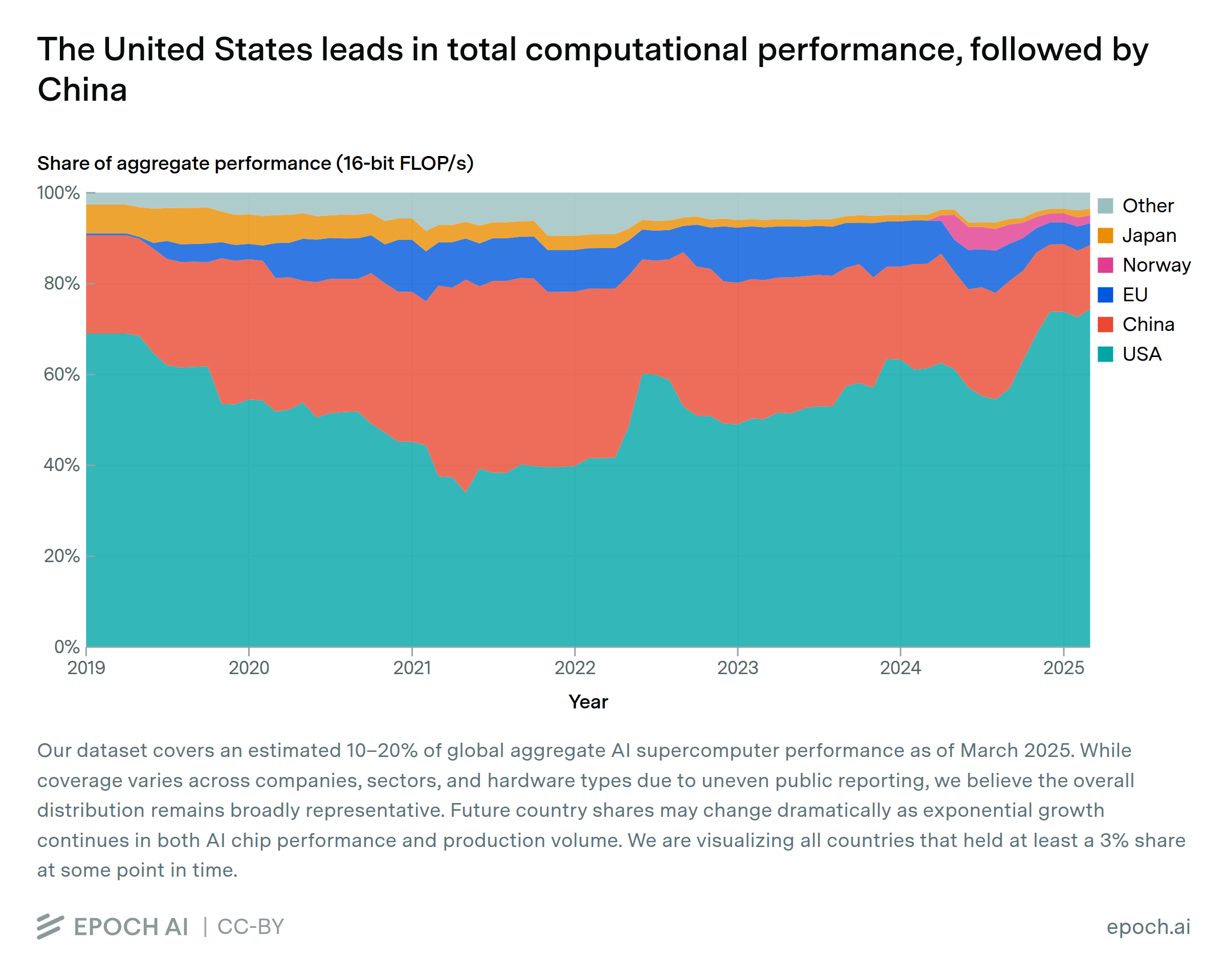

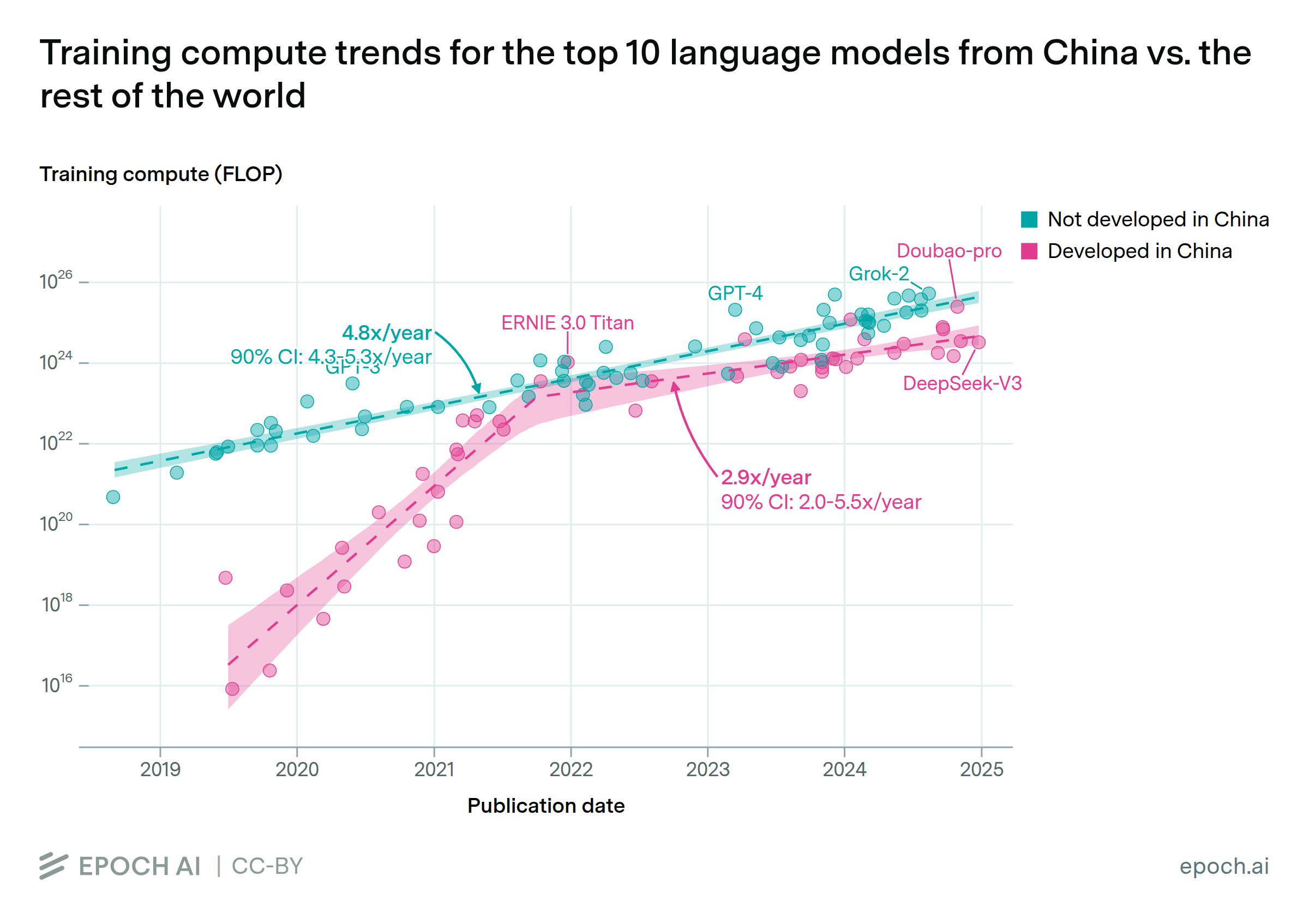

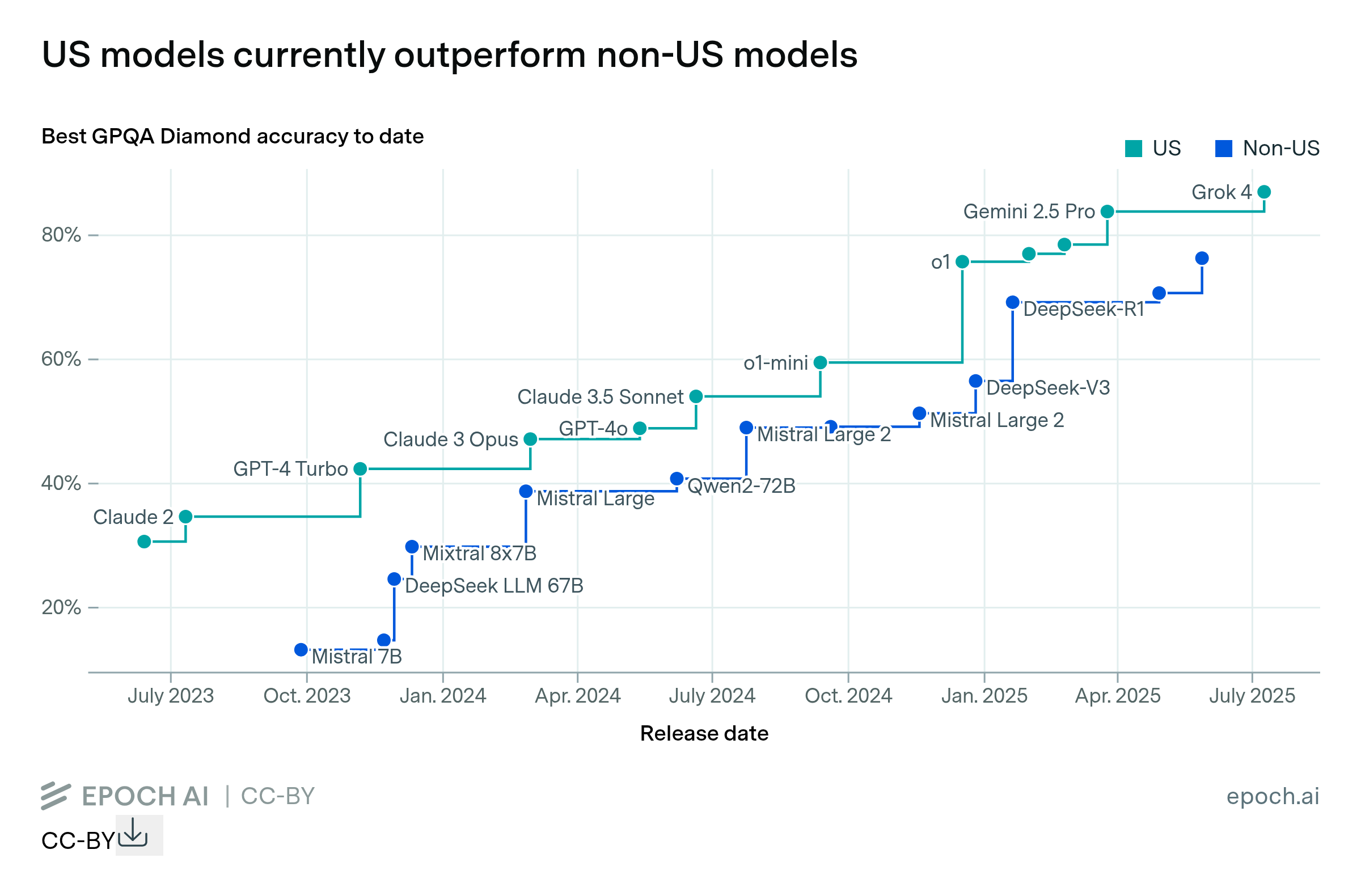

AI development is concentrated in a handful of countries, with the United States and China far ahead of everyone else. Export controls, infrastructure investments, and geopolitics all shape who can build and deploy the most advanced systems. Epoch tracks which countries are leading in AI research and model development, how compute capacity breaks down geographically, and what this means for the global balance of AI capabilities.

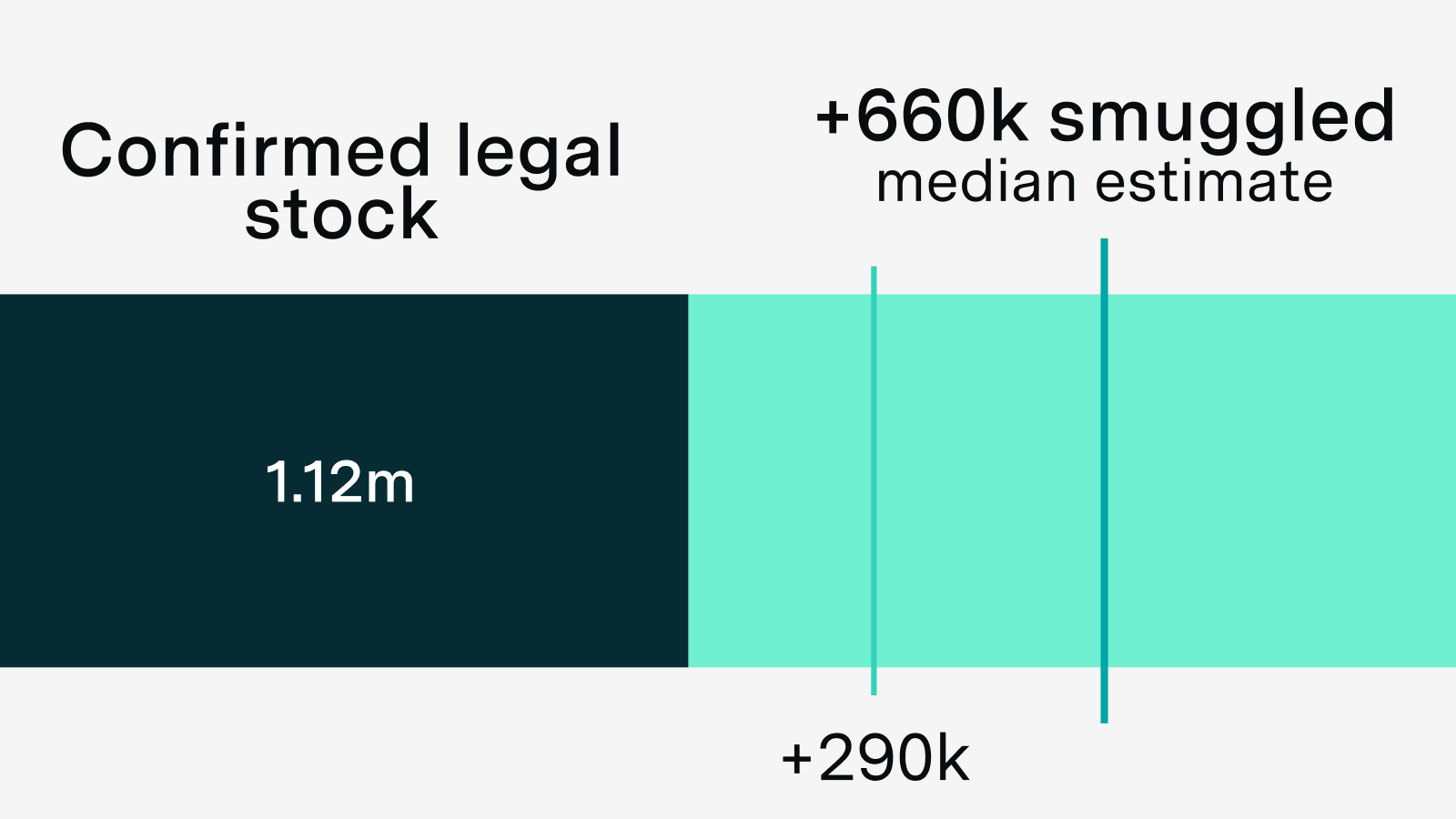

We estimate that between 290,000 and 1.6 million H100-equivalents (H100e) were smuggled to China through 2025. Our median estimate of 660,000 H100e would be roughly a third of China's total compute.

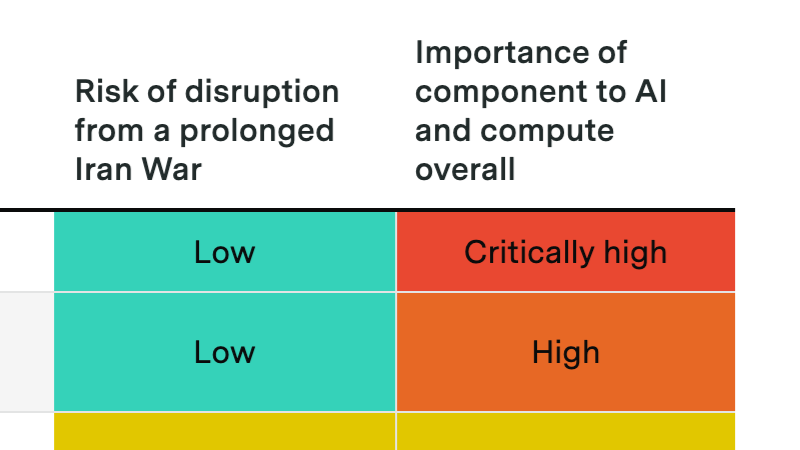

A prolonged Hormuz crisis probably won't derail the compute buildout, but it could slow data center expansion and disrupt Gulf investment flows into AI.

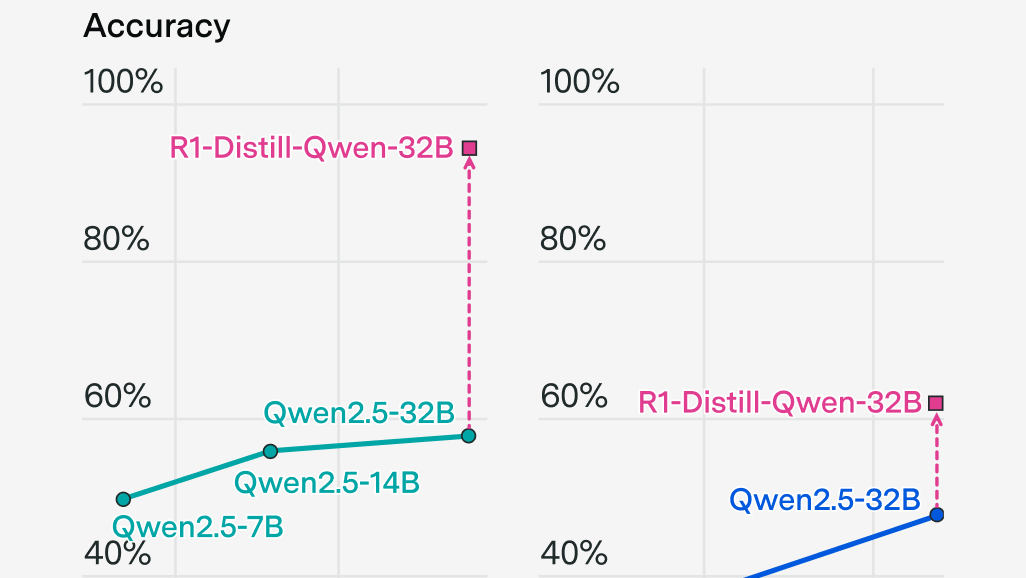

Can Chinese and open model companies compete with the frontier through e.g. distillation and talent?

We announce our new AI Chip Owners explorer, showing which companies own the world’s leading AI chips.

In this episode, economist Luis Garicano chats with the hosts about macroeconomic and labor market effects of AI, with a focus on the EU.

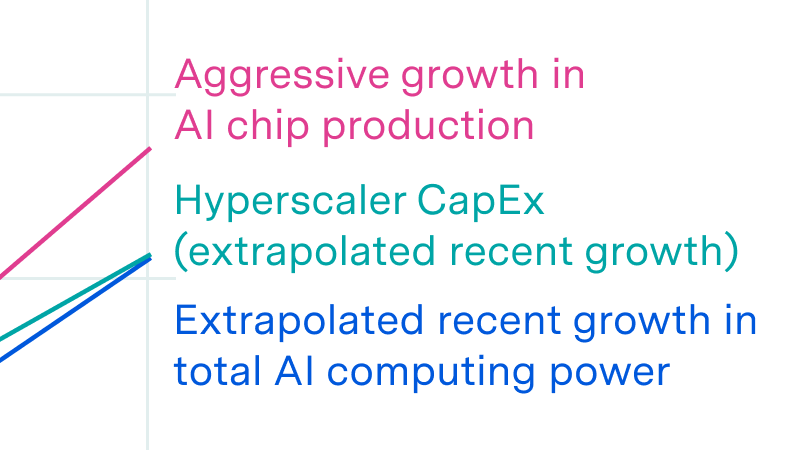

Why power is less of a bottleneck than you think.

'Training compute' is constantly evolving, and compute-based AI policies must adapt to remain relevant

Chinese hardware is closing the gap, but major bottlenecks remain

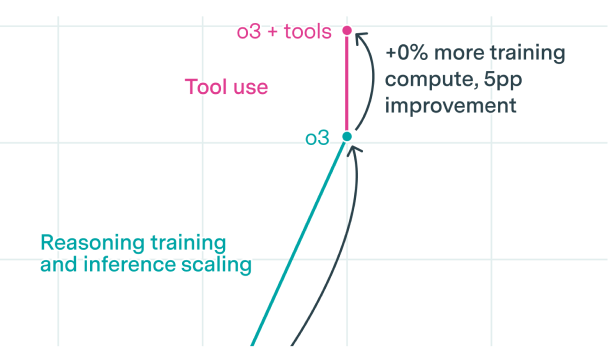

An AI Manhattan Project could accelerate compute scaling by two years.

Export controls on China give the US a hardware lead of around 4 years in training frontier models, but essentially no lead in serving those models to users.

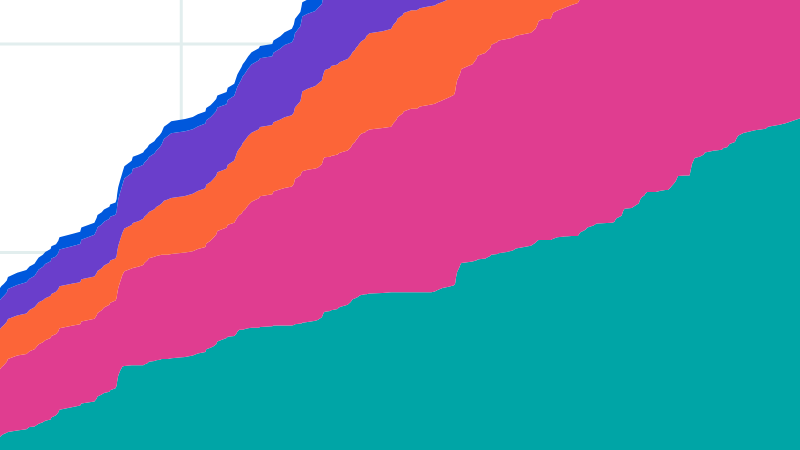

Industry emerged as a driving force in AI, but which companies are steering the field? We compare leading AI companies on research impact, training runs, and contributions to algorithmic innovations.