Key takeaways

- Substantial quantities of AI chips have been sent to China in violation of US export controls. Evidence of diverted or missing chips, drawn from indictments and investigative reporting, points to nearly 300,000 Nvidia H100-equivalents by the end of 2025. This would equal roughly a quarter of the compute China acquired through legal channels or domestic production. Because much smuggling goes undetected, the true total is likely higher.

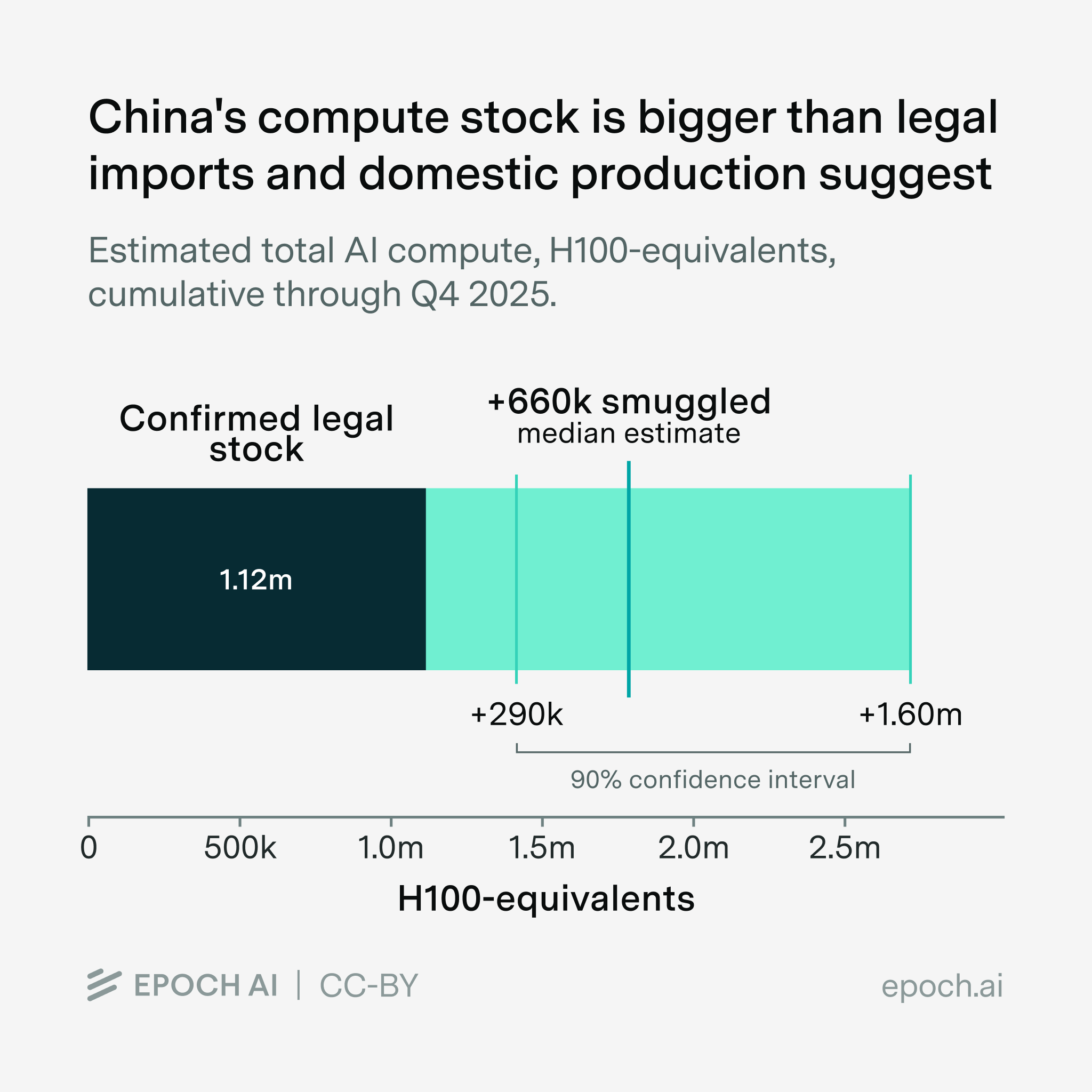

- We estimate, with 90% confidence, that between 290,000 and 1.6 million H100-equivalents of compute were smuggled through the end of 2025. Our median estimate of 660,000 represents roughly 3% of the global compute stockpile, comparable to what xAI, a leading US AI lab, had at the time. The upper bound of our estimate would mean that, by the end of 2025, the majority of China’s AI compute had been smuggled.

- We are uncertain about many variables, notably the magnitude of undetected smuggling and the proportion of chips allegedly diverted or missing that ultimately reached China.

Overview

Over the past several years, the United States has applied multiple rounds of compute-related export controls to China. The earliest rounds of export controls applied to semiconductor manufacturing equipment or to specific entities (e.g., Huawei’s addition to the BIS entity list in 2019). In October 2022, the Commerce Department instituted export controls on all advanced chips with certain characteristics. Commerce tightened these export controls and expanded their scope in October 2023, increasing the incentives for smuggling chips to China. A late 2023 Center for New American Security (CNAS) analysis suggested that the volume of smuggled chips at the time was relatively low, but expected that there would be larger-scale smuggling efforts in the future.

This prediction appears to have been borne out. Investigative reporting by the New York Times, Wall Street Journal, and The Information in 2024 found widespread evidence of banned chips being smuggled into China. In April 2025, Commerce imposed an additional licensing requirement on H20 chips, a type of chip popular in China that Nvidia had developed to comply with prior export controls.1 This further restricted exports and incentivized smuggling. The Financial Times reported that over $1 billion in AI chips were smuggled between April and July.2

Evidence of large-scale diversion by cloud companies has also accumulated. The DOJ indicted several Supermicro employees and arrested a company executive. The employees were accused of diverting $2.5 billion in Nvidia chips to a pass-through entity, which was redirecting those servers to China. Bloomberg investigative reporting insinuates that Megaspeed, a Singaporean cloud provider, has tens of thousands of fewer chips in its Malaysian data centers than it imported from Nvidia, and its CEO is under scrutiny due to close ties to China.

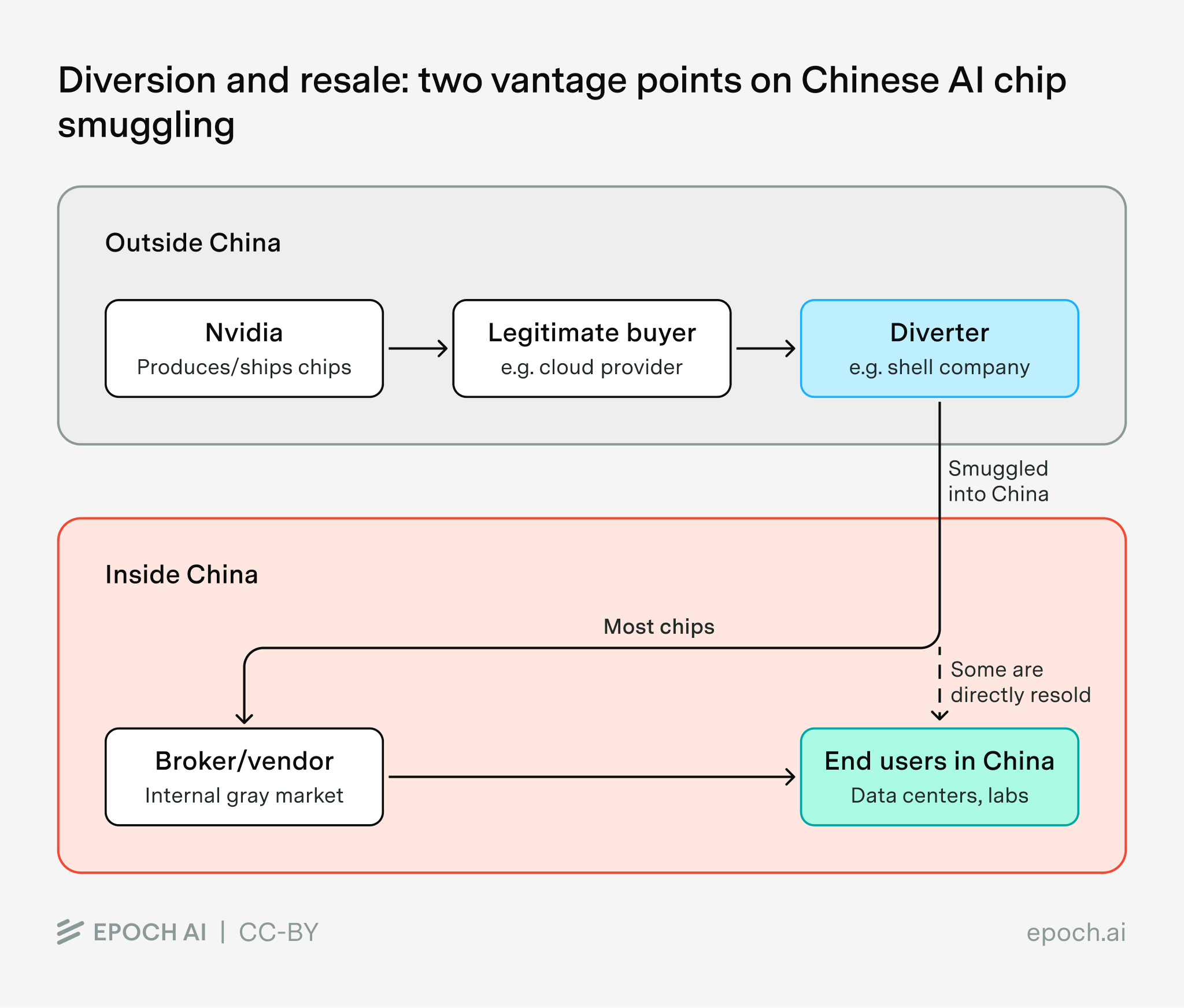

We estimate the total compute smuggled to China using Monte Carlo simulations3 based on evidence from indictments and investigative reporting. We classify this evidence into two types. Diversion evidence traces how chips leave legitimate supply chains and reach smugglers. Resale evidence focuses on the marketplace for smuggled chips within China: the number of vendors or brokers and volumes they transact. Some sources cover both diversion and resale of the same set of chips.

Because every successfully smuggled chip must be both diverted and resold4, we can build two parallel estimates of the same underlying quantity that should, in theory, approximately agree. While our resulting distributions for diversion and resale aren’t identical, they do substantially overlap.

The diversion estimate is created by building a database of allegations from 2024 and 2025, and then adjusting for false or overstated allegations, and for cases missed by reporting and enforcement5. The database does not include cases where diversion was attempted but known to have failed. The resale estimate approximates total volume in the market for smuggled compute by aggregating investigative reporting on vendor counts and the scale of individual transactions. The resale estimate draws on portions of a 2024 CNAS estimate of smuggled compute by Grunewald and Fist.

Cumulative allegations of diverted or missing chips total almost 300,000 H100e6 by the end of 2025 — a quarter of the compute that China is estimated to have legally imported or domestically produced. This figure is neither a ceiling nor a floor on actual smuggling. This figure may overstate actual smuggling for two primary reasons: the allegations are largely not yet proven in a court of law, and some of the chips redirected to China may not have arrived there. Conversely, the 300,000 estimate captures only publicly alleged cases — some, probably most, smuggling goes undetected by journalists and authorities. Thus, we believe it is almost certain that the true total quantity of compute smuggled into China is higher than 300,000. More details and a cumulative summary of reported and alleged smuggling are below.

Our model estimates 660,000 (90% CI: 290,000–1.6 million) H100e of cumulative compute smuggled through the end of 2025. This is somewhat higher than other estimates, including those by CNAS and ChinaTalk, though the median is well within their confidence intervals and vice versa. A comparison against these other estimates, including a discussion of the differences, follows below. Further details on the model and our estimates follow below. Our estimates cover quantities of chips and servers physically moved into China. They do not cover cloud compute located outside of China but used by Chinese customers, an arrangement that, subject to end-use restrictions and sanctions-list screening, is generally permitted under current US export controls. These estimates can be viewed in a global context by checking out Epoch’s AI Chip Ownership Hub.

Evidence on smuggled chips

Compute diversion

Evidence on the redirection of chips to China from outside China primarily draws from public indictments and journalistic investigations into allegations of diversion, though some investigative reporting also provides evidence of resale within China.

A table of cases that are primarily diversion is shown below. Cases that cover both diversion and resale in China are listed in both tables.

| Alleged actor | Type | Chip count | H100e | OEM7 $ (Resale) | Chip model |

|---|---|---|---|---|---|

| Supermicro | Diversion | ~80k | ~141k | 2.5 B | 50% B200 |

| Megaspeed8 | Diversion | 50k9 | ~111k | ~1.7B | 80% B200 |

| Hao Global | Diversion | 177610 | 1776 | H100s | |

| Janford Realtor case | Diversion | 400 | 126 | A100s | |

| ALX solutions | Diversion | ~1600 | ~1600 | H100s | |

| Li Ming | Diversion | ~5600 | ~5600 | 140M | H100s |

| Aperia | Diversion | ~10000 | ~10000 | 250M | H100s |

| Shenzhen merchant | Both | 60 | 19 | A100s | |

| College student | Both | 6 | 1.9 | A100s | |

| Leslie Zhou | Both | ~2k | ~2k | ~50M->(103M) | |

| William11 | Both | 2400 | 2400 | (120M) | |

| Mike | Both | 4800 | 4800 | 180M->(230M) | |

| Totals | ~157k | ~282k |

Compute resale

This is not based on end-users, but rather based on evidence from the marketplace for chips within China, with evidence coming from investigative reporting, including interviews, observations of sale contracts, and photos of smuggled chips physically present in China

It is also likely that some of the same chips are observed on both the diversion and resale side.12

Some journalistic investigations into Chinese chip smuggling do not attempt to enumerate total volumes moved, and instead discuss specific aspects of the distribution network in more detail. A July 2024 WSJ investigation reported that there were more than 70 active distributors on online marketplaces (of which they spoke to 25), but was vague about total volumes (though noting that many sellers had dozens of chips). An August 2024 NYT piece reported finding a similar number of distributors (nearly 100 stores claiming to sell the chips, of which the reporter spoke to 11) and provided some more detail on order volume (one vendor said companies ordered 200 to 300 chips from him at a time, another described a single 2,000 chip order). While the total number of chips explicitly enumerated in each article is low, the overall inference one can make from the reporting is that, in aggregate, there is a substantial quantity of chips being sold, much of it at a small scale.

Much like the FT piece, there is some uncertainty about how much of the supply obtained by the distributors is coming from the large-scale operations versus a network of smaller-scale smuggling that is described in the pieces. We discuss this further under modeled estimates: for now, we turn to aggregating the explicitly reported cases.

Much of the data that we have on the resale market is about the number of vendors in the marketplace and the range of volumes they face, rather than specifically enumerated individual cases.

| Allegations | Type | Chips | H100e | OEM $ (Resale) | Mix |

|---|---|---|---|---|---|

| Leslie Zhou | Diversion+ resale | ~2k | ~2k | ~50M (103M) | |

| College student | Diversion+ resale | 6 | 1.9 | A100s | |

| Shenzhen merchant | Diversion+ resale | 60 | 19 | A100s | |

| William | Diversion+ resale | 2400 | 2400 | (120M) | |

| Mike | Diversion+ resale | 4800 | 4800 | 180M (230M) | |

| >1B during H20 ban (FT, July 2025) | Resale | ~24k | ~44k | (1B) | 55% B20013 |

| Gate of the Era (FT, July 2025) (note: subset of above total) | Resale | (400M) | |||

| “More than 70 distributors… direct contact with 25 of them” (WSJ, July 2024) | Resale | - | - | - | |

| Many sellers, dozens of chips each month (WSJ, July 2024) | Resale | - | - | - | |

| several vendors … mentioned deals involving hundreds or thousands (NYT, August 2024) | Resale | - | - | - | |

| Companies ordered 200 or 300 chips at a time (unnamed vendor) (NYT, August 2024) | Resale | - | - | - |

Estimation methodology

To estimate the total compute smuggled into China from the evidence we observe, we then have to guess at several related parameters on each side of the model.

Compute diversion

The key uncertainties here are:

- What proportion of diverted compute has been detected?

- We don’t know what proportion of smuggled compute succeeded at not triggering an investigation

- There may be ongoing investigations that have not yet been publicized or resulted in an indictment14

- What proportion of allegedly diverted compute made it to China?

- Attempted diversion doesn’t mean successful diversion

- Allegations can be false, as many cases are not yet proven in a court of law

The biggest driver of uncertainty on the diversion side is that we don’t know what fraction of diversion has been observed. The large-scale smuggling schemes detected and reported so far could represent the majority of the volume, or they might be just a small fraction of the total flows. We consider a wide range of detection rates (90% CI: 10–80%; median 25%15). This is higher than some other illicit flows because successfully identifying a perpetrator can provide substantial information about earlier flows. Detection is easier than interception — if a repeat offender is ever caught, this reveals previous transactions.

In addition to uncertainty about detection, there is also some uncertainty around allegations. Even after indictments are made public, there is not always clear information about how many of what kinds of chips were moved when. In the largest indictment to date, the DOJ alleges that $2.5 billion of chips were sent from Supermicro to a front company, which was then sending those chips onwards to China. The indictment only explicitly claims that $510 million worth of servers made it to China (between April and May of 2025), but other quotes from the indictment suggest that the DOJ believes that at least half of the chips made it to China16. From the indictment, we also know that the scheme was alleged to have grown over time and switched to aggressively shipping Blackwells once they became available (in 2026). Accordingly, we include both case-specific uncertainty17 and a small overall reporting-accuracy haircut.

Compute resale

Two uncertainties shape our resale estimate: what the observed vendor data implies about total market volume, and what proportion of smuggled compute flows through resellers detectable by investigative reporters. We address each in turn.

To estimate total marketplace volume, we follow CNAS in multiplying the number of vendors by volume per vendor, but add a hierarchical model where vendors share a market-wide shock but also have individual variation instead of using a single draw of average vendor volume18.

We parameterize the number of vendors as a lognormal with a 90% CI of [38, 150] for 2024 (following CNAS) and a wider [20, 200] for 2025, reflecting uncertainty about whether the marketplace grew or shrank, as there was less reporting that included the number of vendors in 2025. We follow CNAS by generally parameterizing volume per vendor with a 95% CI of [204, 12,000] chips per year. During the H20 ban period (April–July 2025), we use an elevated upper bound of 40,000 chips per year as the 99th percentile to accommodate Gate-of-the-Era-scale operations, which were reported by the FT as moving almost $400 million in chips during that period.

Because we split 2025 into pre-ban, ban, and post-ban sub-periods to accommodate the elevated per-vendor ceiling during the ban quarter, a shared lognormal year-shock (sigma=0.5) is applied to all three sub-periods. This correlation is needed because summing independent sub-period draws artificially narrows the 2025 distribution relative to 2024’s single annual draw. The shock is calibrated so that 2025’s log-scale spread matches 2024’s.

The above estimates of the number of vendors and vendor volumes are based on investigative reporting about sellers and transactions in the Chinese gray market. There are likely some chips that don’t go through the vendors and brokers of this market; instead, their import is arranged by end users. Gray market sellers are to some extent observable because those sellers also want to find clients, whereas it is harder for journalists to obtain information about entirely internal schemes. However, given the robust gray market (selling export-controlled chips is not illegal within China) and since thus far known cases on the diversion side all went through middlemen, we think that the majority of the chips (90% CI 57–96%, median 82%) go through these intermediaries and scale up our estimate of resale accordingly19.

Combined results

Both the diversion and resale sides are attempts to estimate the same underlying quantity: total smuggled compute reaching China. Diversion approaches this from the export side (what is leaving legitimate channels), while resale approaches it from the China side (what is showing up in the gray market). We combine them as a weighted blend, with more weight on the diversion estimate (which has more case-level anchors grounded in indictments with specific quantities).

The diversion side yields a cumulative median of ~530,000 H100e (90% CI: 180,000 to 1.6 million), and the resale side gives ~700,000 (90% CI: 230,000 to 2.3 million). The resale side runs higher, driven by the marketplace model’s fat right tail (the product of uncertain vendor counts and uncertain per-vendor volumes compounds into a wide distribution). The combined estimate is ~660,000 H100e (90% CI: 290,000 to 1.6 million).

Note that the combined distribution is obtained by averaging draws for diversion and resale: since these are both similar right-skewed distributions with higher means than medians, averaging the draws pushes the combined median up (and narrows the confidence intervals).

Comparison to other estimates

There are two main public attempts at making such an estimate: Grunewald and Fist from the Center for a New American Security (CNAS) estimated 140,000 chips smuggled to China in 2024 (code), with substantial uncertainty around the point estimate (90% CI from 20,000 to 800,000 chips). Their modeling strongly inspired the compute resale portion of our model.

In April 2025, ChinaTalk analyst Aqib Zakaria estimated (code) that cumulatively 452,000 H100e of compute (90% CI: 194,000 to 1.3 million H100e) had been smuggled into China in circumvention of export controls. This estimate built on the CNAS 2024 figure to project 2025 volumes. This estimate used the aforementioned CNAS 2024 smuggling estimate as a starting point for creating a 2025 smuggling estimate.

Our estimates are fairly close, especially on chip count. There is more divergence on the H100e estimate. In 2024, compared to CNAS, we estimated a higher proportion of smuggled chips are H100s/H200s rather than A100s (~83% Hoppers instead of ~67%). In 2025, compared to ChinaTalk, we estimated a higher proportion of smuggled chips are B200s/B300s rather than H100s, with roughly an even split for the year. There is both diversion and resale evidence on substantial quantities of Blackwells making it to China - the Financial Times’ investigation into smuggling during the H20 ban described Blackwells as the most sought after and widely available chip model. The Supermicro indictment confirmed B200 diversions starting in April, and the purportedly missing Megaspeed chips seem to be mostly Blackwells.

| Chip count | CNAS | ChinaTalk | Epoch |

|---|---|---|---|

| 2024 | 136k [17k–772k] | — | 169k [66k–440k] |

| 2025 | — | 216k [123k–388k] | 280k [110k–751k] |

| Cumulative | — | 378k [191k–1,012k]20 | 466k [211k–1,086k] |

| H100e | CNAS | ChinaTalk | Epoch |

|---|---|---|---|

| 2024 | 103k [13k–599k] | — | 159k [64k–419k] |

| 2025 | — | 312k [176k–565k] | 480k [189k–1,289k] |

| Cumulative | — | 452k [194k–1.3M] | 663k [294k–1,593k] |

Quarterly extrapolation

We produce quarterly estimates of compute smuggled in 2024 and 2025.

For 2024, we allocate the annual estimate across quarters using H100 production volume, lagged by one quarter — this captures the expected vendor ramp-up over the course of the year as chip supply grows and more sellers enter the market. The resulting Q1–Q4 weights are roughly [0.18, 0.23, 0.27, 0.33]. For 2025, we allocate based on the pre-ban / ban / post-ban structure used in the resale model.

Conclusion

Our central estimate is that roughly 660,000 H100-equivalents have been smuggled to China through the end of 2025, with substantial uncertainty (90% CI: 290,000 to 1.6 million). At the lower end, smuggling is a meaningful but secondary channel, and most chips moving in violation of export controls have already resulted in an indictment or at least an investigation. At the upper end, smuggling exceeds legal channels as a source of AI compute within China.

A big driver of this range is how much smuggling never surfaces. A 10% detection rate and a 80% detection rate imply very different totals, and the available evidence does not allow us to choose between them with confidence. The evidence from the robust gray market within China helps tighten our confidence intervals, though they remain wide.

It is unclear what the future holds: smuggling increased from 2024 to 2025, but this was partially driven by changes in export controls that increased incentives to smuggle chips. On paper, export controls have loosened again, though the impact on legally shipped chips is uncertain. The recent disruption of several major smuggling operations may also contribute to decreased diversion flow.

Acknowledgements

Thanks to Amelia Michael, Aqib Zakaria, Erich Grunewald, Cheryl Wu, Konstantin Pilz, Tim Fist for their helpful feedback.

-

China had imported almost 18 billion dollars worth of H20’s, around 220,000 H100e’s worth, between their 2024 introduction and their ban.

-

While the H20 restrictions were lifted by the US in July 2025, China subsequently restricted H20 imports. While the initial lifting of the restrictions appeared to reduce demand for gray market chips, it is unclear whether gray market sales rebounded when H20 sales did not resume.

-

Simulations that involve repeatedly drawing random values for each uncertain input to build up the distribution of possible outcomes.

-

In some cases, the end user may be directly arranging for the diversion of the chips, typically through a shell company or other pass-through entity. We then consider the transfer of the chips from the pass-through entity to the end user to be the resale step. It is possible that some chips may be smuggled in more directly by the end-user, but we anticipate that this is small in proportion to total flows.

-

We assume reporting is accurate with a median of 80%, 90% CI (61-94%) and that the detection rate is between 10-60% (90% CI), with a median of 24.5%. In addition to an overall reporting discount, for each case, there is case specific uncertainty about whether purportedly missing or attempted diverted chips made it to China.

-

Compute capacity in the equivalent number of Nvidia H100s, based on dense 8-bit operations per second.

-

OEM $ is Original equipment manufacturer price - resale rates could be 1.5x-2x higher and are sometimes included in parentheses when provided by the source

-

Megaspeed and Company-1 in the Supermicro indictment appear to be different companies. Reporting suggests that Megaspeeds suppliers are Aivres and Nvidia directly.

-

“Since its founding in 2023 through November of this year, Megaspeed has imported Nvidia hardware worth at least $4.6 billion, containing at least 136,000 Nvidia graphics processing units, or GPUs” … “Across the sites, Nvidia cataloged Megaspeed-owned servers and racks equivalent to some 86,000 GPUs.”

-

Believed to have reached China, per the plea deal

-

“When the broker who calls himself William was arranging the $120 million order for the Chinese electrical appliance company, the order was so big that it triggered a mandatory on-site inspection by personnel from Nvidia, who wanted to ensure that the costly equipment was properly installed.”

-

For example, it is unclear what proportion of the smuggled chips observed by the Financial Times in their mid-2025 reporting on smuggling during the H20 ban period overlapped with the chips covered by the total in the subsequent Supermicro employee indictment. Supermicro was repeatedly mentioned throughout the FT piece as an assembler whose products were popular on the black market, in particular the large scale reseller Gate of the Era which purportedly did $400 million of sales. However, the piece also mentions Dell and Asus products without further specifying proportions. Even if we knew what share of the billion dollars of servers were from Supermicro, we still couldn’t be sure what proportion were servers that were smuggled by the defendants through the specific shell company referenced in the indictment versus which were independently smuggled by smaller scale resellers (examples of which were documented by other news investigations).

-

“Nvidia’s B200 has become the most sought-after — and widely available”

-

For example, there was a long gap between then the BIS placed a hold on Supermicro shipments to “Company-1” and when the indictment brought these allegations to public light

-

This estimate is influenced by evidence from tax evasion (25% detection) and corporate fraud (33%), the financial fraud component makes this more analogous than drug smuggling.

-

“Company-1 did not have the capacity to store or use the massive quantities of servers it was purchasing from the U.S. Manufacturer, and most of the servers it ordered at the direction of the defendants were instead diverted to China through a network of third-party brokers who worked closely with the defendants.” (source)

-

For example, since an indictment is stronger evidence than investigative reporting, we model Supermicro as having between 1.25B-2.5B worth of servers diverted to China, while we model Megaspeed as has having between 0 and 50,000 chips (mostly Blackwells) diverted to China

-

This falls between drawing a single “average volume” from the distribution of observed vendor annual rates (which produces unrealistically wide bounds) and independent draws for each vendor (which produces unrealistically narrow bounds). These modeling options all have the same average volume.

-

Even company-internally organized procurement of chips would still count as resale under this taxonomy, as Chinese companies would need to set up shell-companies to buy the chips and then “sell” them back to the parent company.

-

Our attempt at summing CNAS 2024 and ChinaTalk 2025 numbers

About the authors

Related work