What’s going on inside Chinese AI companies like Alibaba and DeepSeek? Western observers usually answer this question in two ways: (1) read through their technical papers, and (2) voraciously consume news reports and follow everything about Chinese AI on X. But there’s a third approach that people have rarely explored: scrape Chinese AI job postings.

Chinese labs need to hire the right people, so in their job descriptions they need to reveal what skills or expertise they’re looking for. These give us direct clues into what constraints they face and what they hope to build.

So like we previously did for Western labs, we scoured over 1,600 job postings across six of the most notable Chinese AI companies: DeepSeek, MiniMax, Moonshot, Z.ai, ByteDance, and Alibaba. Here’s what we found.

Chinese AI labs still rely on Nvidia, but they’re exploring domestic alternatives

Many people care about whether Chinese companies still use Nvidia because it means they still depend on “Western” AI infrastructure. And at least for now, that seems true.

Consider ByteDance. One of its open roles is called “Inference GPU Performance Optimization Expert”. Whoever gets hired for this would be responsible for ByteDance’s flagship LLM inference framework, and importantly, they’d manage this using Nvidia’s CUDA software. Per the job description:

“Primarily through GPU and CUDA performance optimization techniques, combined with real-world production conditions, build an industry-leading, high-performance LLM inference engine.”

It also explicitly calls for using TensorRT-LLM, which is a software library for LLM inference, optimized specifically for Nvidia GPUs. So that’s a smoking gun for “ByteDance still uses Nvidia chips in inference”.

But another role suggests that ByteDance is pushing beyond Nvidia. ByteDance Seed has a job posting for an “AI heterogeneous computing optimization expert”, which says this:

“Those with knowledge of optimizations related to inference/training/communication using Ascend, Cambricon, etc., and experience in high-performance operators, large-scale training, and converged computing will be given priority.”

Unlike the previous example, mentioning these other chip lines is instead a smoking gun for “ByteDance is looking into other kinds of compute”. And this isn’t just a speculative future direction — Z.ai’s role brags about how they’ve already trained GLM-Image end-to-end on domestic chips (emphasis ours) earlier this year:

“In early 2026 the team developed and open-sourced GLM-Image and GLM-OCR. The former is Zhipu’s new flagship image-generation model, trained entirely on domestic chips”

So maybe they’re looking to hire more people who can do similar things, bringing them closer to independence from the Western AI chip ecosystem. But these job postings don’t tell us how much closer they are — we’d need to know the numbers on how much compute they have and how it’s used.

Our best guess is that Chinese labs use domestic chips pretty frequently for inference, but rarely for pre-training large models. The exceptions are post-training large models or training small models like GLM-Image. This has 16 billion parameters, which is probably 10–100× smaller than their largest models.

Chinese startups are renting domestic cloud compute, and building data centers too

We’d really like to know where Chinese AI labs get their compute, because that’s (arguably) what matters most for AI progress. Labs that use more compute develop better AIs, and to know which labs these are, we need to trace things back to the source.

The most obvious source is to rent cloud compute. Similar to how OpenAI rented cloud compute from Microsoft Azure, Chinese AI startups can scale by renting from domestic cloud providers like Alibaba and ByteDance. For example, Moonshot has a job posting for procuring cloud compute resources.1

But Chinese startups are increasingly following in the footsteps of their US counterparts by building their own data centers. Old Chinese tech titans like Alibaba and ByteDance have operated these for a while, but startups are now joining the fray. For example, MiniMax has a job posting looking for top STEM talent, which says this:

“4. Participate in building company-level self-built data centers and the SRE & DevOps system, ensuring the reliability of multiple core systems.”

Similarly, we saw a DeepSeek job posting about a data center role in Inner Mongolia, and a related posting did the rounds on X:

And Moonshot also put out a job posting for procuring data centers. More generally, it looks like they’re following a hybrid approach with both cloud compute and data center buildouts. Another job posting from Moonshot explicitly calls for applicants to help with this: “coordinate the hybrid deployment/rollout of public cloud and self-built intelligent computing centers”.

Chinese AI startups have pretty varied commercial strategies

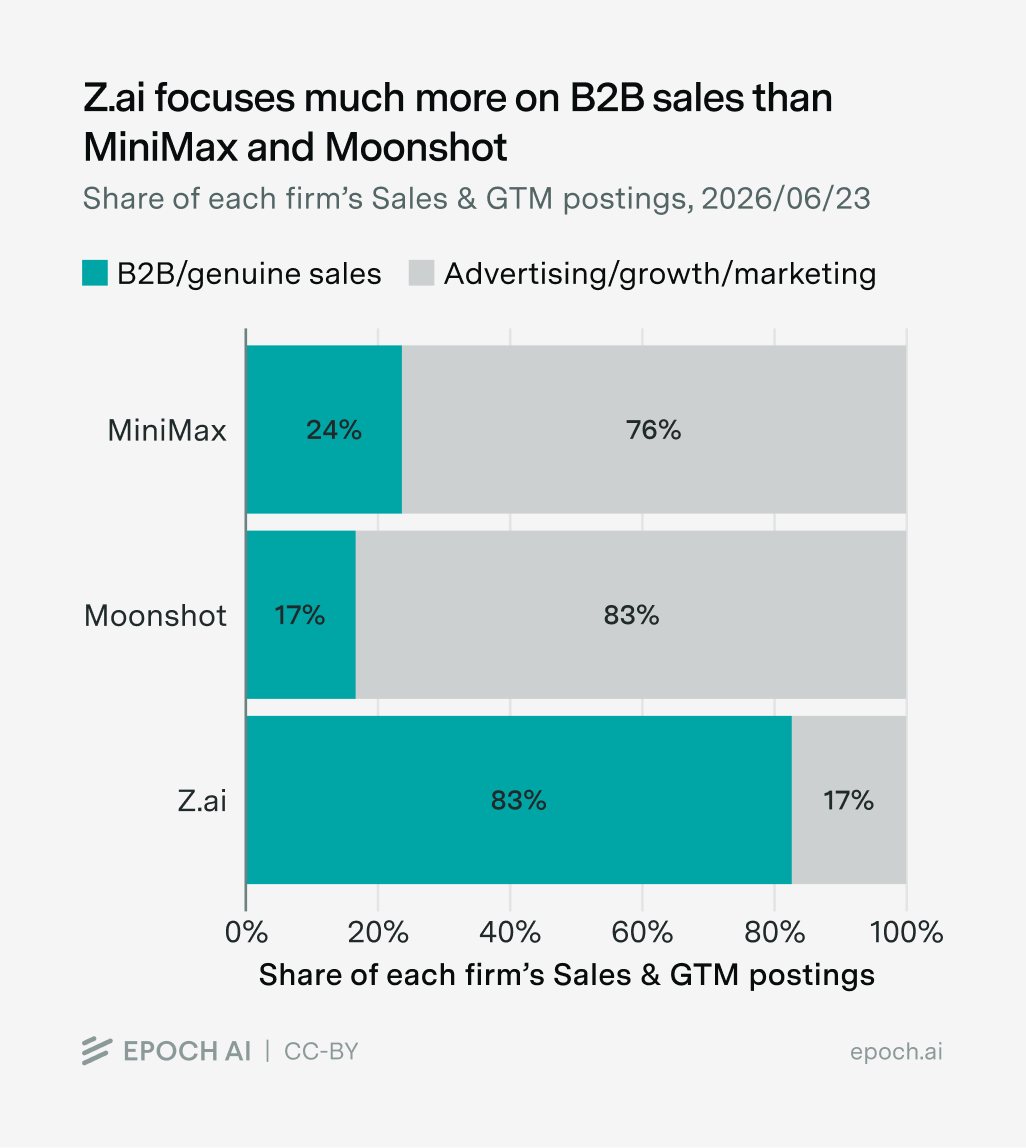

You know how Anthropic focuses more on B2B sales compared to OpenAI? Well you see this pattern among Chinese AI startups too — just replace “Anthropic” with “Z.ai”, and “OpenAI” with “MiniMax and Moonshot”.2

One way to see this is to tally up the job postings aimed at finding and selling to customers, or “go-to-market”. For Z.ai, most of these roles are about B2B sales, whereas for MiniMax and Moonshot it’s mostly about marketing:

This isn’t so mysterious if you know about the revenue structures of these companies. Around 70% of MiniMax’s revenue in 2024 and 2025 came from AI-native products to individual consumers, like its Talkie “companion AI” app, or its video generation service Hailuo. The remaining 30% came from enterprise sales. In contrast, 73.7% of Z.ai’s 2025 revenue came from running models on its customers’ infrastructure — one of the heaviest-touch B2B sales approaches out there.

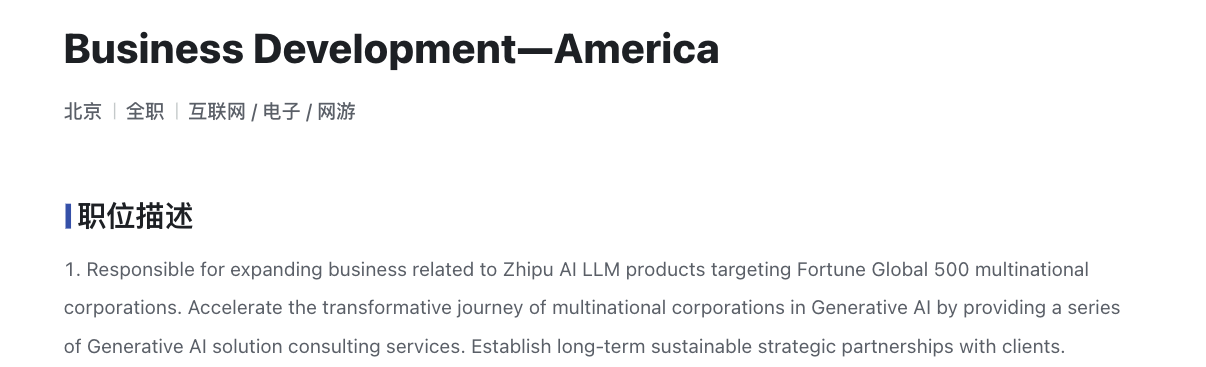

Who are these enterprises? Some of Z.ai’s job postings highlight government institutions and state-owned enterprises — including in energy and finance — as target clients. They also have roles that focus on US market expansion, specifically eyeing Fortune Global 500 companies:

That said, Z.ai still isn’t that internationally focused, at least compared to MiniMax. The latter has 16 active postings in San Francisco, as well as more in Hong Kong, London, Singapore, Dubai, Berlin, Tokyo, Seoul, Madrid, Mexico City, and Île-de-France. And this matches what we know from financial reports — 73% of MiniMax’s 2025 revenue came from international markets, compared to 9.8% from Z.ai.

Startups stay model-centric; platform companies make a wider range of research bets

Another thing to look at is companies’ product strategies. This tells us what they care about and what constraints they’re facing. So what are they building?

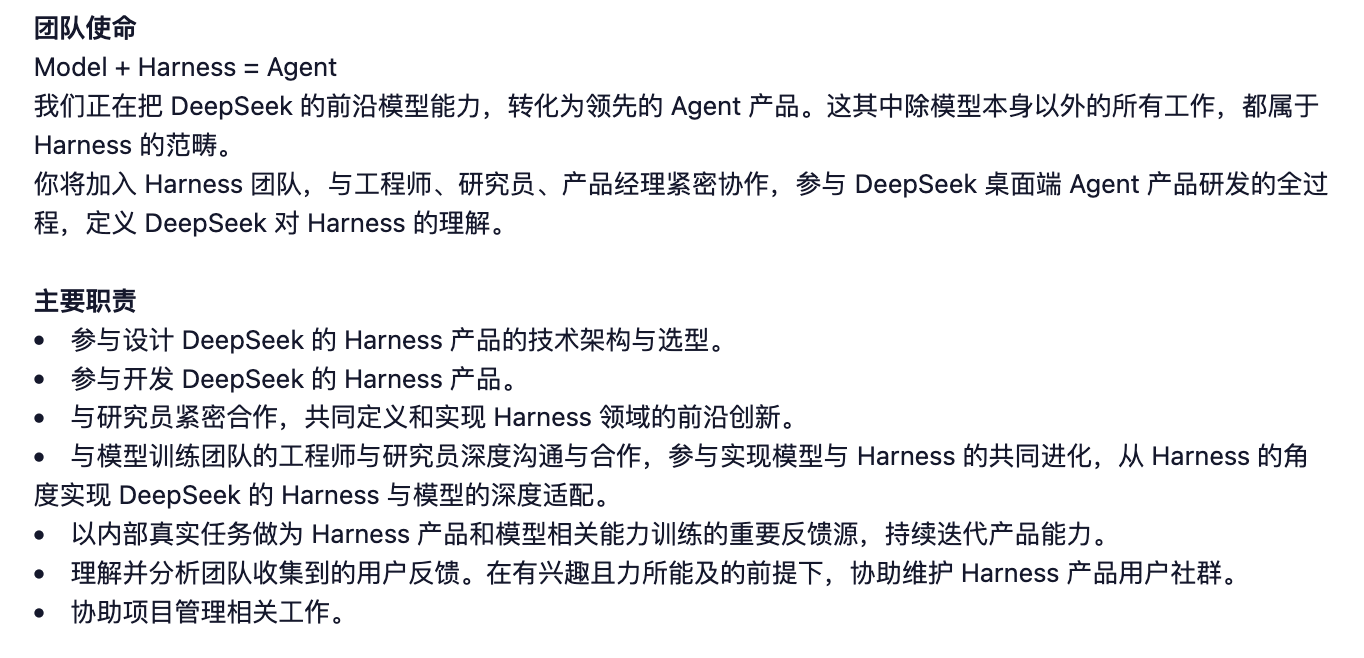

Postings from startups like DeepSeek and Moonshot tend to focus narrowly on improving LLMs, or building products on top of them. Consider the following job description — it has so much English in it you can broadly tell what it’s about even if you don’t read Chinese:

Unsurprisingly, this role is called “Agent Harness R&D Engineer”.

Z.ai similarly focuses on LLMs, though they also have two job postings on robotics. These are part of its new X-Lab research unit, which focuses on exploring novel research frontiers, like new model architectures.

Finally, there are the big established players, who reach far beyond the realm of software. ByteDance and Alibaba both have roles in robotics and wearable hardware.3 Alibaba’s Qwen team also has a specific role that focuses on automotives, where the hire would be “responsible for core algorithm R&D and technical deployment of the Qwen cockpit voice-assistant AI Agent”.

Why the different strategies? Our answer is that this just boils down to the advantages of various labs. Large platform companies are better placed to build lots of real-world physical stuff, because they’ve already secured a strong foothold in the relevant supply chains, and they have more leeway to make big research bets. Startups instead have to narrow their focus and lean into building great software.

Job postings are more spread out than in the US

If you want to work on frontier AI in the US, the Bay Area is the most obvious place to be. But if you want to work on frontier AI in China, where do you go?

The answer is one of a few big tech hubs, namely Beijing, Hangzhou, and Shanghai. This is pretty clustered — 93% of all the postings with stated locations are based in at least one of these three hubs. The biggest hub is Beijing, which was listed in 63% of the postings.

Each bubble is a mainland-Chinese city; its area is proportional to the number of open job postings located in that city, pooled across six Chinese AI firms, as of June 23, 2026. A posting that lists several cities is split equally among them (a posting in N cities contributes 1/N to each), so the bubbles sum to the total number of postings at a location rather than double-counting multi-site roles.

But this agglomeration isn’t at the level of the US, where about 85% of the job postings at frontier AI labs are based in San Francisco alone.4 Part of the reason for this difference may be lots of competition among Chinese provinces, which subsidize local companies to get their own provincial champions, naturally leading to more hubs. It might also be driven by fountains of strong talent streaming out of China’s top universities, especially in Shanghai, Zhejiang, and Beijing, so companies want to headquarter themselves there.

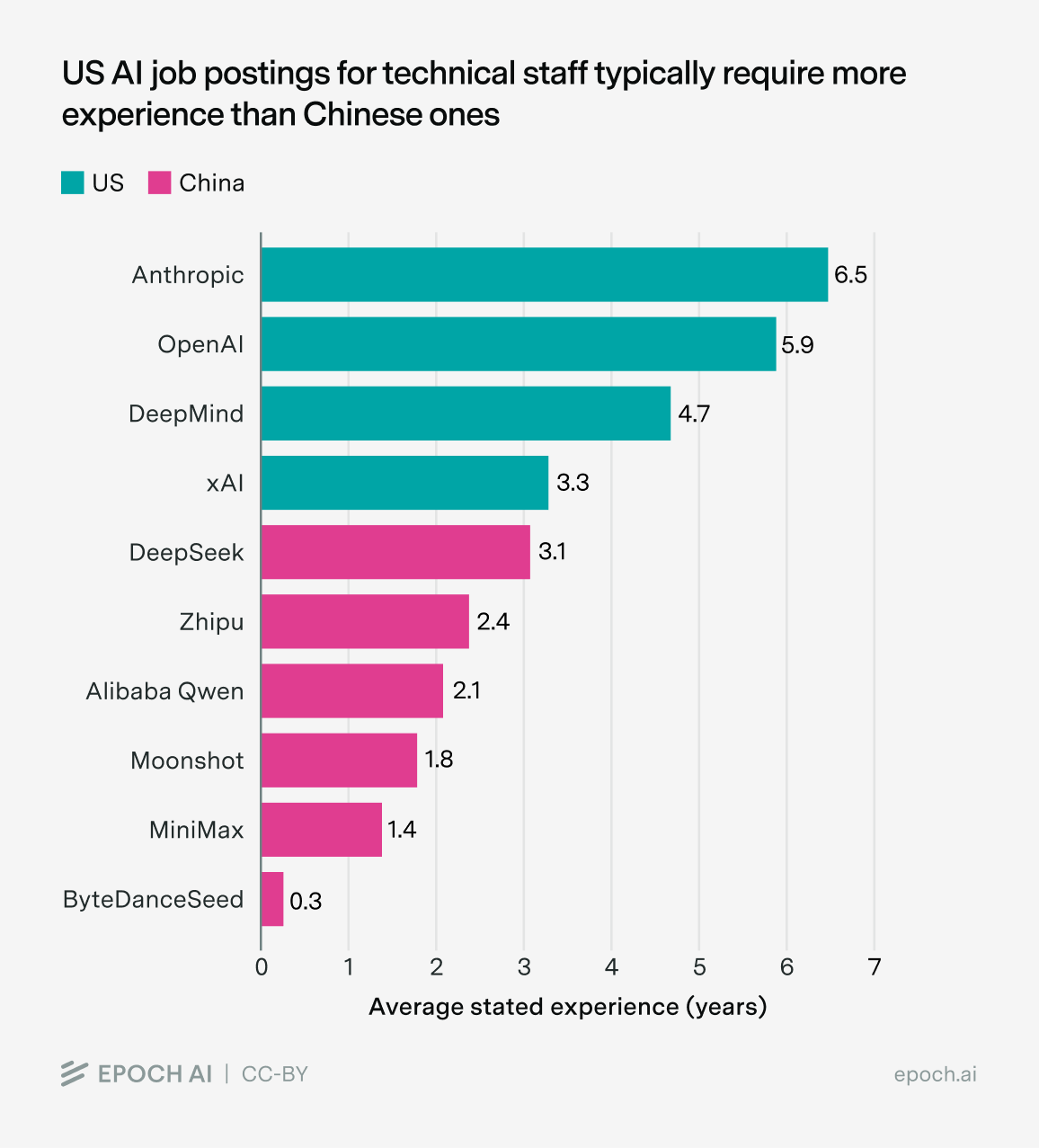

Chinese AI jobs require less prior experience

One of the most striking differences between Chinese and American AI job postings is the amount of prior experience you need to apply. US labs required 5.5 years on average, compared to just 1.6 years among Chinese ones.5 The US labs are looking for far more seasoned applicants.

Each bar is the mean of the minimum years of prior work experience required across a firm’s technical staff job postings, from a single snapshot of the firm’s careers site on June 23, 2026 (N = 1,258 postings with an experience requirement across ten firms).6

Part of the difference is institutional. The Chinese government urges universities to treat campus recruitment as the main channel for graduate employment. Their Ministry of Education in turn runs recurring campaigns, which among other things aim to “provide every job-seeking graduate with at least 5 job listings”.

Founders seem to have embraced this with open arms. DeepSeek’s CEO Liang Wenfeng has said that the firm “hires on ability, not experience”. ByteDance also has a recruitment program called “Top Seed”, which explicitly targets current students and recent grads. In contrast, this hiring approach might actually violate the law in the US:

Given this, it’s perhaps no surprise that campus postings account for nearly 20% of the open engineering roles in our data on Chinese labs.

The complex reality of Chinese AI firms

When we look at the online discourse about frontier AI labs in the US, we often think of them as having their own complexities and “personalities”, even if they’re competing on similar dimensions. Anthropic seems big on AI safety and embodies a worldview where “code is all you need”. OpenAI is famous for being the creator of ChatGPT, and seems interested in AI as a truly general-purpose technology. Google’s thing is AI for science, and it’s often seen as having an edge on compute. xAI defies all expectations about when and where you can build data centers. Regardless of your opinions on these companies, their strategies and cultures can vary quite a bit, and it’s worth understanding the differences.

These job postings tell us that the same is true for Chinese AI firms.7 Like Anthropic, Z.ai seems to care more about B2B sales, at least compared to other Chinese AI startups. Big Chinese tech giants focus on a variety of products beyond LLMs, like robotics and wearable devices. And Chinese labs see a very different industry landscape compared to US firms, which pushes them to explore domestic alternatives to Nvidia and focus on hiring from universities, across multiple big AI hubs.

So Chinese AI labs aren’t all following the same playbooks. They have to deal with their own market challenges, and they have to find their own solutions. These details are worth paying attention to — even if that means reading the descriptions of jobs that we’ll never apply for.

Appendix

| Area | DeepSeek | Moonshot (Kimi) | MiniMax | Z.ai (Zhipu) | ByteDance (Seed) | Alibaba (Qwen) |

|---|---|---|---|---|---|---|

| Coding / coding agents | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 Website 2 | — None | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 | ✓ Yes Website 1 Website 2 |

| Roleplay / companion | ✓ Yes Website 1 | — None | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 | ✓ Yes Website 1 | ✓ Yes Website 1 |

| Robotics / embodied | — None | — None | — None | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 Website 2 |

| AI for Science | — None | — None | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 Website 2 |

| Automotive / smart cockpit | — None | — None | — None | — None | — None | ✓ Yes Website 1 Website 2 |

| Multimodal / AIGC generation (image·video) | — None | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 |

| Voice / speech | — None | ✓ Yes Website 1 | ✓ Yes Website 1 | ✓ Yes Website 1 | ✓ Yes Website 1 Website 2 | ✓ Yes Website 1 |

| AI hardware / wearables | — None | — None | — None | — None | ✓ Yes Website 1 | ✓ Yes Website 1 Website 2 |

We’d like to thank Isabel Juniewicz, Lynette Bye, Stefania Guerra, and Campbell Hutcheson for helpful feedback and support on this post.

-

At this point, some of our DC policy readers will be asking, “but how much of this is foreign cloud compute?”, because that’s a loophole in compute export controls. Unfortunately we didn’t see anything on this in the job postings — sorry!

-

We only analyze Moonshot, MiniMax, and Z.ai here because these three firms operate as relatively independent AI startups, so their job postings reflect commercialization decisions for their AI products more honestly. By contrast, Seed and Qwen are research teams whose sales and marketing decisions might be delegated to their parent companies, namely ByteDance and Alibaba respectively. DeepSeek has HighFlyer backing it, and it also only has one sales job posting among its 47 job postings.

-

Interestingly, Alibaba’s robotics role mentions “Passion for artificial general intelligence (AGI) and the future of robotics” as a source of bonus points for prospective hires.

-

For the sake of this post, “leading foundation model labs” include OpenAI, Anthropic, xAI and Google DeepMind. This is based on previous work looking at AI job postings.

-

These numbers assume zero years of experience, if no experience requirement is stated. But the US-China gap in required prior experience persists even if we restrict ourselves to postings that give an explicit figure — 5.5 years for US labs compared to 3.4 years for Chinese labs.

-

Required experience is parsed from job postings in both English and Chinese. If a range is given, we use the lower bound, and where both languages state a figure, the Chinese one is used. A posting is included in a firm’s mean if it states an experience requirement, or is a campus recruitment posting (which we assume means zero years of required experience). We exclude postings that state no requirement and aren’t based on campus-recruitment.

-

Also, it’s more common for random non-AI companies in China to build pretty good LLMs from scratch, though this isn’t something that we saw explicitly from the job postings. For example, Meituan (think Chinese DoorDash + Yelp + Uber Eats + more, but combined) has developed their own 560 billion parameter mixture-of-experts model, with reasoning abilities.

About the authors