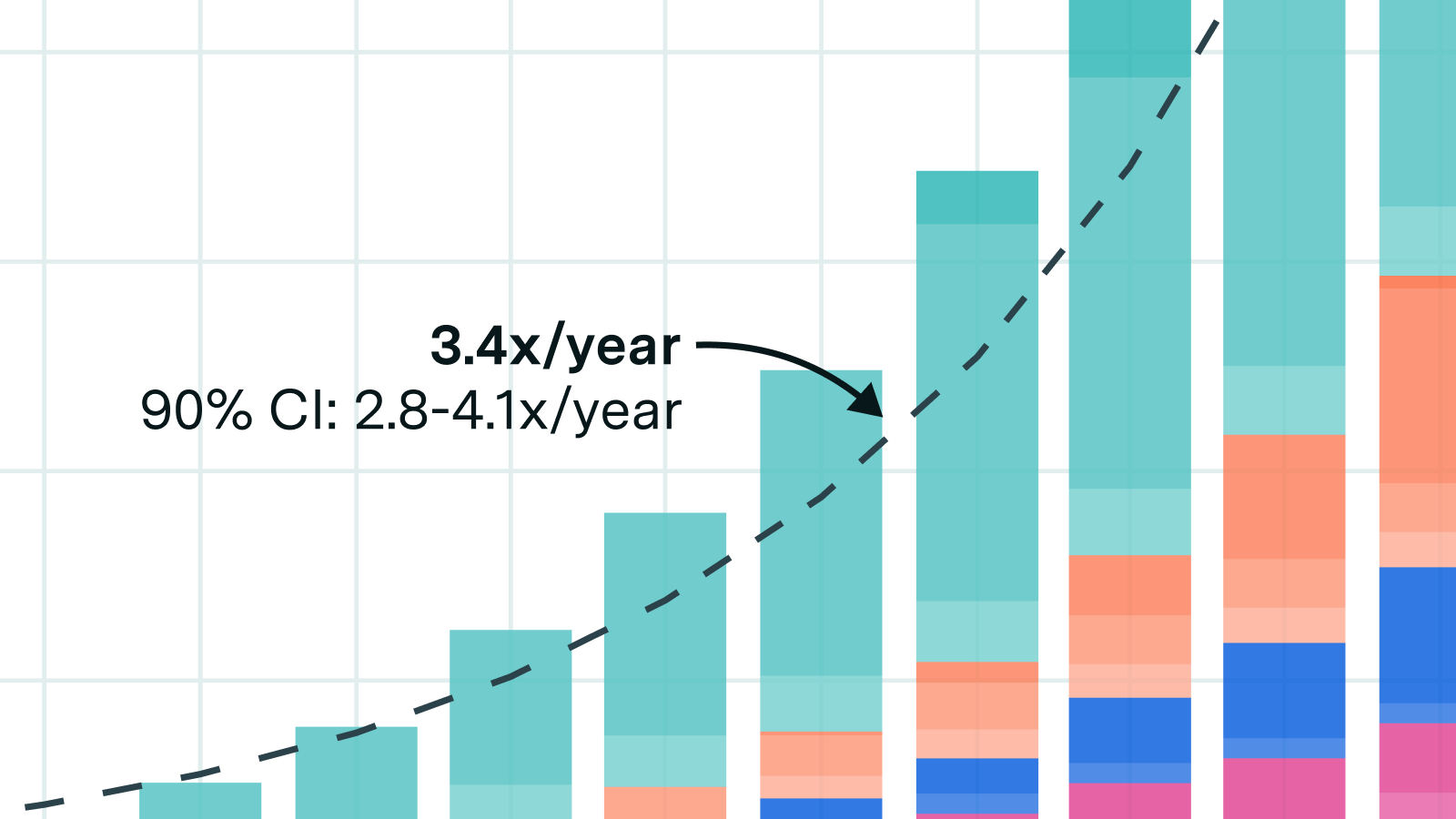

Driven by investments in AI infrastructure, the combined capital expenditures at Alphabet, Amazon, Meta, Microsoft, and Oracle have been growing at an average of 72% per year since the second quarter of 2023. If this trend continues, they will spend $770 billion in 2026.

Company statements and analyst projections anticipate continued rapid spending growth in 2026, though slightly slower than naive extrapolation. Our data is sourced from companies’ financial filings and includes cash spending and new finance leases. This growth rate is consistent with the spending growth we observe in our AI chip sales dataset.

Epoch's work is free to use, distribute, and reproduce provided the source and authors are credited under the Creative Commons BY license.

Learn more about this graph

We sum quarterly capital expenditure across Amazon, Microsoft, Alphabet, Meta, and Oracle using two components extracted from SEC filings: (1) cash PP&E (cash payments for property, plant, and equipment) and (2) finance lease ROU assets obtained (right-of-use assets obtained in exchange for finance lease liabilities, effectively new leases). Where these exact tags are unavailable, we use the closest available tag or combination of tags. We then fit an exponential model to the post-Q2 2023 data to characterize the growth rate.

Data

Analysis

Limitations

Related insights