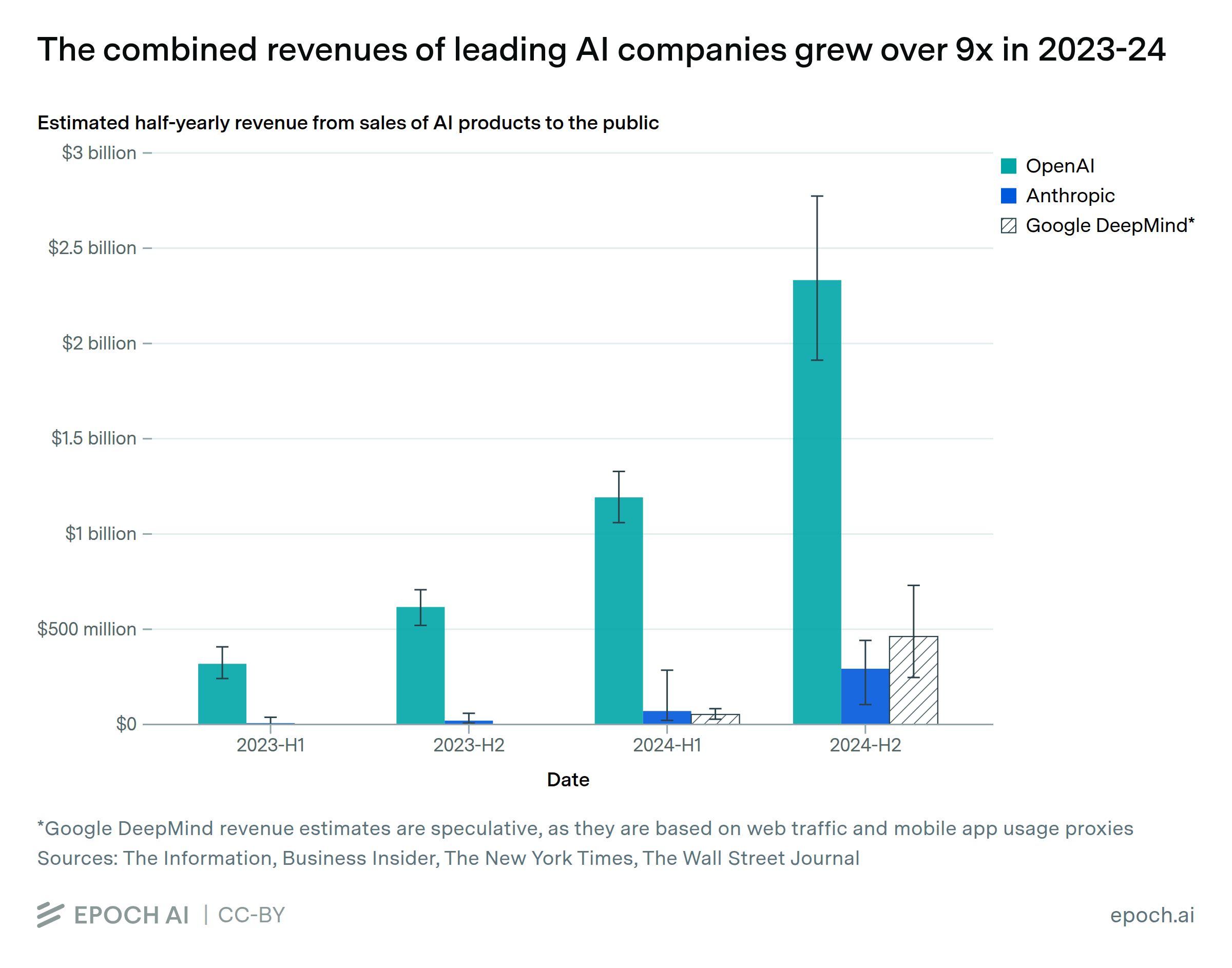

OpenAI, Anthropic, and Google DeepMind each grew their revenue over 90% in the second half of 2024, corresponding to an annualized growth over 3x/year. OpenAI’s and Anthropic’s revenue projections both imply that their revenue will continue to grow over 3x in 2025. Projecting to April 2025, we estimate OpenAI’s revenue at around $10B/year, while Anthropic and Google DeepMind each earn single digit billions per year. Note that our estimates for Google DeepMind are more speculative, and don’t include internal revenues from integration with Google products, which could be substantial.

According to our estimates, no other AI company surpassed $100 million in revenue in 2024 by selling access to their own models. However, companies such as Microsoft and Amazon collectively make more revenue than top AI companies by charging for access to third-party models. Microsoft alone reports $13B in revenues from its AI business, seemingly driven by sales of Copilot (which uses OpenAI models).

Epoch's work is free to use, distribute, and reproduce provided the source and authors are credited under the Creative Commons BY license.

Learn more about this graph

We estimate half-yearly revenues from leading AI companies selling access to their models. We focus on OpenAI, Anthropic, and Google DeepMind, as these are the companies where we estimate highest sales revenues. We estimate that other AI companies made less than $100 million in revenue in 2024.

For OpenAI and Anthropic, we fit exponential trends to revenue numbers from media reports. For Google DeepMind, we compare web traffic and mobile app data for Gemini with the same measures for ChatGPT and Claude.

Note that our estimates capture only revenues from external customers that companies generate with their own models. This means we don’t include internally generated value (e.g. potential improvements to Google Search via the “AI Overview” feature), or revenue from third-party models (e.g. Microsoft’s revenues from selling OpenAI models via Microsoft Copilot). We also ignore revenue streams that are not primarily generated by AI products (e.g. research agreements).

Code to reproduce our analysis is available here.

Data

Analysis

Assumptions

Explore this data

AI company data, with data on revenue, funding, staff, and compute for many of the key players in frontier AI.